How to Know How Much Property Taxes You Paid

Citizen's Guide to Belongings Taxation

- Assessment Process

- Budget Process

- Property Tax Bills

What is the purpose of property taxes?

Property taxes are a primary source of funding for local regime units, including counties, cities and towns, townships, libraries and other special districts including fire districts and solid waste districts. Holding taxes are administered and nerveless by local government officials. These funds are used to pay for a variety of services including welfare; constabulary and fire; new construction and maintenance of buildings; local infrastructure like highways, roads and streets; and the operations, including salaries, of the local units of government.

Property taxes are an ad valorem tax, meaning that they are allocated to each taxpayer proportionately co-ordinate to the value of the taxpayer's property. The statewide average acquirement distribution for each belongings revenue enhancement dollar is as follows:

- County: $0.nineteen

- Township: $0.03

- Metropolis/Town: $0.24

- School: $0.42

- Library: $0.04

- Special Unit of measurement: $0.07

Breakdown is based on average expenditure per dollar of property tax levied in Indiana for taxes payable in 2018. (Data sourced by the Section.)

The belongings revenue enhancement process is as well known every bit the property tax assessment and billing bike. This wheel begins with the development of each property's assessed value past the county assessor. The assessor then transfers the data on each property'due south value to the county auditor. The auditor, afterward applying deductions, exemptions, and other valuation adjustments, sends these values (known equally the certified net assessed values) to the Department of Local Authorities Finance. After thorough review, the Department converts these values to property tax rates by dividing each local unit's approved upkeep amounts by the assessed value for each unit. The Section forrard these rates back to the county, where the auditor and treasurer piece of work together to calculate, generate and mail tax bills to each taxpayer. Acquire more about the assessment to budget procedure.

The Department's website offers a diverseness of resources to brainwash and inform taxpayers on this process. The site also features search tools to provide taxpayers with sales disclosure and assessment data on properties statewide. This information can be used in the appeals process or to permit taxpayers to better understand how assessors determine a holding's assessed value.

Cess Process

How is the value of my property determined?

The tax assessment and billing cycle begins with the assessor's valuation of your property. Only like other states, in Indiana properties are valued using mass appraisal techniques. With mass appraisal, your belongings is looked at in conjunction with other properties in your area. Assessors consider age, form, and condition. Finally, in a process known as annual adjustment, or "trending", each year real property sales data is used to make up one's mind if the value of backdrop in your area should change to match the market value found in the sales of recent backdrop.

(Prior to 2002, property was reassessed every 5 to x years. That left taxpayers with a large alter in their assessments between reassessments, which often led to sudden increases in property tax bills.)

Learn more about Annual Adjustment and Reassessment.

What role does the DLGF have in the belongings tax assessment process?

The Section plays several roles related to property valuation and assessment. The primary function of the Section is an oversight role. After the assessor has placed values on all properties in a county, the assessor submits to the Department an assessment to sales "ratio written report" for review and approving. The ratio report is basically a comparison betwixt sales and assessed values in the county to ensure that market values are beingness used to determine assessed values. The Department uses several statistical tests to make up one's mind whether assessed values are in line with property sales in the area. Tests are also run to ensure that the assessments are fair and care for all property owners equally. Once these tests are passed, the assessment work in the county is approved.

In add-on to oversight activities, the Department is responsible for the cess of certain types of railroad and utility belongings. To learn more than about this procedure, click hither.

How do I know how much my property is worth? What if I don't hold with my belongings's value?

You volition receive notice of your holding'southward value in one of 2 ways: the county assessor may send yous a notice of assessment, known as a Course xi. Otherwise, the assessed value of your holding can be constitute with your tax nib. This document is known as the TS-1 tax comparing statement.

If you feel your cess does not reverberate the market value-in-use of your property, you may appeal your assessment. To file an appeal, you lot must contact your local assessor past June xv of the year that you recieve a Form 11. If no Form 11 is mailed, the filing date it June xv of the post-obit year. Indiana law does not require taxpayers to submit an appraisal in order to appeal an assessment.

To come across an illustration of the property tax cess appeals procedure, click here.

Budget Process

How are belongings tax rates determined?

Property taxes represent a property owner'south portion of the local authorities's budgeted spending for the current twelvemonth. Increases or decreases depend upon a local authorities's fiscal management, the assessed valuation of a property and/or local revenue enhancement rates, which are based on the budget proposals submitted by local government taxing entities that provide services to each community. Local spending is the reason for property taxation charge per unit increases - or decreases - depending on local fiscal direction.

Each twelvemonth, local units (or the municipal or county fiscal body responsible for adopting a unit's upkeep, rates, and levies) submit their adopted upkeep to the Department. The Section and then reviews each unit of measurement's budget, and ensures that the upkeep is in line with laws, regulations, and other property revenue enhancement controls related to this spending. After the unit makes whatsoever necessary adjustments, the Section approves a funded budget and develops tax rates for each taxing unit.

What kind of budget review does the Department practise?

Essentially, the Section ensures that the proposed spending of the local government unit does non exceed the unit's property taxation paycheck. If the proposed spending does exceed the unit'southward predictable holding tax paycheck, the unit of government is required to revise its budget to bring it in line with the paycheck. In this way, the Section works in a way that is similar to a bank. The bank will tell its client how much money is available in an account, only not how to spend the money. Information technology is the aforementioned human relationship between a local unit of measurement of government and the Department.

What are local taxing units and taxing districts?

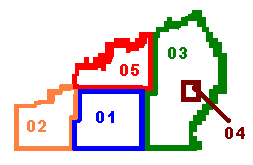

A taxing unit is an individual unit of regime with the authorization to levy property tax. Examples include township, cities and towns, counties, fire service, school corporations and libraries. All of the combined taxing units that provide services to a common geographical area compose a taxing district. Beneath is an example of a county (in this case Ohio) displayed with its taxing districts:

What is the difference between a taxation rate and a tax levy?

A taxation rate is the per centum used to determine how much a belongings taxpayer will pay per one hundred dollars of net assessed value. A tax levy is the amount, specific in dollars, that a taxing unit (city, boondocks, township, etc.) may raise each year in property tax dollars. In other words, the levy is the cap on the amount of property tax dollars a local government is allowed by law to collect.

How is the tax levy determined?

The amount each unit is allowed to collect each year is based on the unit'southward "maximum levy," which is based on the amount of holding taxes raised past the unit concluding year. Additionally, state law allows a unit of measurement of government to enhance more levy than in the previous year. The amount by which the levy can increase is called the growth factor. A unit has the option of requesting the maximum levy or a lesser levy each year. If a unit chooses not to take its maximum levy in a given year, the unit's overall maximum levy is not impacted.

How is my local taxation rate determined?

Each unit's levy is calculated and so a rate is determined by the Section. This is done by dividing the unit's levy by its net assessed value.

Tax Rate = Total Tax Levy / (Total Net Assessed Value/100)

To illustrate this, we tin refer back to the Ohio Canton example. Each unit has its ain tax charge per unit. The sum of these rates for each commune equals the total tax rate. For Commune 01, the breakdown is as follows:

A more than basic way of understanding the human relationship betwixt the levy, net assessed value and the revenue enhancement rate is in terms of a gift purchased by a group of people. If five people are going to pitch in coin to purchase a gift, and the full cost of the souvenir is $100, each person will have to pay $xx. If the number of people willing to pitch in on the gift suddenly drops to 4 people, each person will pay $25. If the four people decide to purchase a different gift for simply $80, so the amount each person pays is even so the aforementioned. If the cost of the gift increases to $125, and the number of people pitching in drops to four, each person will have to pay $31.25. This is the aforementioned relationship that exists between certified net assessed value (the people), the property tax levy (the toll of the souvenir), and the tax charge per unit (the corporeality each person pays).

How can I become involved in the local budgeting process?

The offset step in becoming involved in the local budgeting process is to assemble information. The Department has assembled the educational tools found on this website that tin assist y'all begin to sympathize the intricacies of local regime financing and the budget procedure in general. In addition, taxpayers tin likewise find canton by county detail on belongings revenue enhancement related matters, including how many property tax dollars are being collected and used in each county.

Public local budget hearings are usually scheduled in September and October to comply with a statutory borderline for all taxing units to adopt budgets by November 1 of each yr. After the political subdivision formulates its estimated budget and its proposed tax rate and tax levy, each political subdivision volition give notice to the taxpayers stating the time and place set for the public hearing to discuss the estimated budget and tax levy. This notice is published twice with the get-go publication at least ten (x) days before the date fixed for the public hearing. This is an opportunity for the public to annotate on the political subdivision's budget, tax charge per unit and tax levy. If 10 (10) or more taxpayers object to a budget, tax rate or tax levy of a political subdivision, they may file an objection petition with the proper officers of the political subdivision not more seven (seven) days after the public hearing. If an objection petition is filed, the political subdivision shall prefer with its budget a finding apropos the objections in the petition and any testimony presented at the adoption hearing. (November 1 is the statutory deadline for a political subdivision to prefer a budget, revenue enhancement charge per unit and tax levy.)

Property Tax Bills

How is my tax bill calculated?

In concept, the adding of a tax bill is fairly unproblematic - multiply the assessed value of your property after deductions by your local taxation rate and that is your gross tax liability. There are, nonetheless, many other steps that can brand the process more complicated.

Every bit an example, let's say your primary residence in Cass Township, Ohio County is valued by the assessor's office at $200,000. This is known as your gross assessed value. All the same, you may be eligible to receive deductions on your property that would reduce your tax liability. Since this is your primary residence, you lot may be eligible to receive the Homestead Standard Deduction (the bottom of $45,000 or lx% of the gross assessed value) and Supplemental Homestead Deduction (35% of the remainder value up to $600,000; 25% of the remainder value exceeding $600,000). For example purposes, presume that the unabridged value of this property is owing to a homestead - a dwelling, ane garage and upwardly to ane acre of existent estate.

$200,000 - $45,000 -$54,250 = $100,750

The property's value after deductions are practical - in this case, $100,750 - is known as your net assessed value and is the value upon which your tax pecker will be calculated.

In gild to calculate your tax nib, your net assessed value is multiplied by your local tax rate of $0.7090. (In Indiana, revenue enhancement rates are calculated on a per $100 basis. This ways that, for every $100 your abode is worth, yous are charged lxx.9 cents.)

($100,750/100) x $0.7090 = $714.32

This is your total revenue enhancement bill for the year. Information technology can exist further reduced by the addition of belongings revenue enhancement credits, which are subtracted directly from your billed amount.

Since this is a homestead property, the property tax caps will prevent you from paying more than ane percentage of the gross assessed value in property taxes.

$200,000 x 0.01 = $2,000

Since your tax bill of $714.32 already is below the maximum of $2,000 you volition not receive an boosted credit related to the belongings tax caps. If your taxation bill, after the application of other credits, had exceeded the maximum, an additional credit would have been applied to reduce the nib to the maximum amount determined under the property taxation caps.

When are belongings taxes due?

Property taxes should be due in two installments annually - one on May 10 and 1 on Nov 10. At least xv days prior to May 10, the county treasurer is required to mail to each taxpayer the TS-1 belongings revenue enhancement beak and comparison statement.

What penalties will be applied to my property taxes if I fail to pay by the engagement they are due?

If an installment of real property taxes is completely paid on or earlier the engagement 30 days subsequently the due date and the taxpayer is not liable for delinquent property taxes first due and payable in a previous installment for the same packet, the corporeality of the penalty is equal to five% of the amount of runaway taxes. Otherwise, the amount of the penalty is equal to 10% of the amount of runaway taxes. As well, with respect to property taxes due in two equal installments, on the twenty-four hours immediately post-obit the due dates of the first and second installments in each year following the year of the initial delinquency, an boosted penalty equal to 10% of whatever taxes remaining unpaid will exist added. A belongings may become subject field to a tax sale if the taxes remain unpaid (IC vi-1.1-24-1).

What types of property revenue enhancement relief are bachelor to taxpayers?

- Exemptions - an exemption is a total or partial waiver of property tax liability for a given holding. Exemptions are generally only available in express circumstances, such as for not-for-profit organizations, religious groups, and economic development purposes.

- Deductions - a deduction is a subtraction of assessed value for a property prior to the calculation of tax liability. Deductions are the almost common types of belongings tax relief available to taxpayers and include relief for principal residences (homesteads), mortgaged property, veterans and disabled citizens, to name a few.

- Credits - a credit is a type of holding taxation relief applied direct to the tax liability subsequently it is initially calculated. Common property tax credits include the circuit breaker credit and the local property revenue enhancement replacement credit.

For more data about holding revenue enhancement bills, see "Understanding Your Revenue enhancement Bill" which is available from the left-hand navigation links on the Department's website.

Source: https://www.in.gov/dlgf/understanding-your-tax-bill/citizens-guide-to-property-tax/

0 Response to "How to Know How Much Property Taxes You Paid"

Post a Comment